Henry Seymour

The Fallacy of Marx's Theory of Surplus-value

I.—On Commodities, and the Nature of Value.

III.—The Double Function of Money.

V.—Contradiction of the Theory of Capital.

VI.—Labor-Power as a Commodity.

To the Memory of

Pierre Joseph Proudhon,

These lines are Dedicated.

“While many admit the abstract probability that a falsity has usually a nucleus of reality, few bear this abstract probability in mind, when passing judgment on the opinions of others.”—Herbert Spencer.

Introduction.

The disciples of Karl Marx claim that their master’s greatest achievement was to bring to light the important “generalisation” of surplus-value. This pretended generalisation, which is set forth with a great flourish of “scientific” demonstration in the pages of Das Kapital, is in reality the economic cornerstone of State Socialism. It is the pretext which is put forward by the Social Democrats as a reason d’être, as a sort of moral justification, for the establishment of that reactionary measure which has been euphemistically described as the collective ownership of the means of production, exchange, and distribution.

In passing, we have abundant proof, from a study of comparative Ethnology, that this idea of collective proprietorship has prevailed amongst all primitive peoples, and of historic data there is ample to warrant the conclusion that it is only since the idea has grown into comparative desuetude, that industrial and economic progress has been possible. Moreover, it is easy to trace the root cause of present economic inequality and its manifold evils to so much of the same idea as still survives, by which means the State is permitted to interfere with the industrial activities of the people and prevent the freest access to natural opportunities of wealth-production and consumption. Are we therefore not justified in the interference that the revival of “collectivism” at the present day is nothing more than a manifestation of social atavism?

Marx claims that his theory of surplus-value furnishes the key to the inequitable distribution of wealth. The object of this treatise is to expose the extravagance of such a claim, and to point out—I believe for the first time—that this theory of surplus-value is based upon two antithetical hypotheses, upon two ideas which are mutually exclusive. I shall shew that Marx’s theory of surplus-value is a complete contradiction of his theory of value, of which it is pretended to be a logical corollary; for the theory of value involves that the use-value of a commodity does not enter into the exchange-value thereof, whereas the theory of surplus-value rests entirely upon the contrary assumption that it is the alienation of the use-value by the laborer of his “commodity”, labor-power, that enables the capitalist to increase its exchange-value, and thereby acquire a surplus-value.

Furthermore, to include labor-power, as Marx does, in the category of commodities, is a complete begging of the question. In this again he is in contradiction with himself. For in the very beginning of his book he tells us in plain and unmistakable language that a commodity is an object upon which labor-power has been expended. He elsewhere declares that a commodity is essentially a value-bearer, and that “human labor-power in motion, or human labor, creates value, but is not itself value. It becomes value only in its congealed state, when embodied in the form of some object.” If value is not anterior to the product of labor, how it can become a quality of mere labor-power passes all comprehension. We shall furthermore discover that the “value” of labor-power is but a figurative expression. As Proudhon said: “When, by a sort of ellipsis, we say the value of labor, we make an enjambement, which is not at all contrary to the rules of language, but which theorists ought to guard against mistaking for a reality. Labor, like liberty, love, ambition, genius, is a thing vague and indeterminate in its nature, but qualitatively defaced by its object,—that is, it becomes a reality through its product. When, therefore, we say, This man’s labor is worth five francs per day, it is as if we should say, The daily product of this man is worth five francs.” When Marx includes labor-power in the list of commodities, he simply confounds cause and effect.

To maintain the extraordinary proposition that labor-power is a commodity, and that its value is governed by the same law that governs that of other commodities, Marx was at a loss to supply a single fact or argument. He simply took for granted the antiquated theory of wages put forward by M. Turgot, in his “Reflections on the Production and Distribution of Wealth”, and afterwards defended by Ricardo,[1] a theory to which Lassalle gave the metaphorical designation of the “iron law”. It is very certain that this theory of wages has no foundation in fact. Is it not axiomatic that the natural price of labor is the total product thereof? Is this not a law which theoretically admits of no exception? And if the laborer’s needs of subsistence fixed the price of labor as a matter of fact, should we not expect to find at all times and places a uniform scale of wages? For are not the needs of all laborers virtually the same? But we certainly find no such thing. As Adam Smith says, “in almost every part of Great Britain, there is a distinction, even in the lowest species of labor, between summer and winter wages. Summer wages are always highest. But on account of the extraordinary expense of fuel, the maintenance of a family is most expensive in winter.” And how can it be reconciled with this “iron law”, that in England and America, where the economic evolution is most advanced, and values are more generally fixed, wages are higher, nominally and really, than in those countries, such as China, Russia, Spain, and Italy, which lag far behind in the economic march? According to the theory, wages in the former should be lower than in the latter countries, whereas the facts indicate that the exact opposite is the case. Again, it will be conceded that wheat is the staple food of the laborer. Well, let us glance at the following figures. According to Tooke, the price of wheat in 1812 was 118s. the quarter, while according to Mulhall, the average weekly wage of the artisan was 20s. In 1852 wheat had fallen to 41s. the quarter, and yet wages remained stationary. If the “iron law” were true, wages would have fallen pari passu, the more so as the shrinkage in prices was more or less general.

Marx failed to perceive the effects of legal monopolies upon normal economic phenomena, and consequently supposed that the exploitation of surplus-value was to be ascribed to the private ownership of land and capital. Following this supposition he held that the general introduction of machinery was immediately responsible for that lack of employment of and competition amongst laborers which operate to bring down wages to “the subsistence limit.” Here again he is clearly in error. For it is only since the introduction of machinery that the laborer’s standard of comfort (real wages) has risen to any sensible degree; his enlarged opportunity of consumption is due almost entirely to those mechanical miracles, to those tireless cogs and wheels, which have wrought such glorious revolutions in the industrial world, and which have made labor so productive and wealth so abundant. In the middle of the eighteenth century, when Arkwright brought his loom into the spinning industry, there were 5,000 persons employed at the wheel. Now there are 500,000 persons employed in this industry. Here is evidence of an increase in the demand for labor a hundredfold in one industry alone, thanks to machinery; which is to be accounted for by the increased productivity lowering prices, enlarging the sphere of consumption, making, in turn, this additional employment of labor possible.

In the following chapters I shall attempt to prove that the whole train of Marx’s reasoning was vitiated by an ignorance of the rôle of money in distribution.

I.—On Commodities, and the Nature of Value.

We are to consider that mysterious trinity in unity—use-value, exchange-value, and surplus-value. Inasmuch as the scope of these pages is confined to a refutation of the theory of surplus-value promulgated by Karl Marx, I shall traverse only those chapters of Das Kapital which the necessity of the case requires, and in quoting therefrom, I shall employ the English translation made by Samuel Moore and Edward Aveling from the third edition of the German.

Marx begins the first chapter of the first volume with the observation that the sum total of wealth in capitalist society is an immense collection of commodities, of which the single commodity is its elementary form. He then very properly points out that in order to discover the laws that govern the distribution of wealth, it is necessary to first analise the elementary unit, and he straightway proceeds to subject the commodity to theoretical dissection.

He says: “A commodity is, in the first place, an object outside us, a thing that, by its properties, satisfies human wants of some sort or another...The utility of a thing makes it a use-value.” It is an object, he tells us, upon which human labor has been expended, and which at the same time possesses the quality of satisfying some human requirement, some real or fancied need. This latter quality he calls, after Adam Smith, the use-value of a commodity, in contradistinction to its exchange-value. Ergo, air, water, sunlight, are indispensable; yet, since they cost the laborer nothing, since they are the free and spontaneous productions of Nature, they have no exchange-value whatever.

Furthermore, a thing may be useful and be also a product of labor, and still not be a commodity. For the object of the production of commodities is exchange, and consequently it is not enough that they have utility for the actual producer; they must have a social use-value, a use-value for others.

A commodity therefore, is:—

(1) An object possessing social utility; and

(2) An object upon which labor has been expended.

Marx next proceeds to shew that it is labor, and labor alone, which is the common element in the whole range of commodities, and which fixes by a general law, the relation of exchange-value between one commodity and another. The social use-value of a commodity, he tells us, merely determines its exchangeability, whereas its exchange-value is governed by the amount of labor necessarily consumed in its production.

But what is meant by the amount of labor? Labor is an abstract quantity. Whence arises, therefore, a unit of measurement? The aptitudes of men are so variable that one man may be able to produce in one day a concrete result equal to that which another may require two days to accomplish.

Marx says:

“The total labor-power of Society, which is embodied in the sum total of the values of all commodities produced by that society, counts here as one homogeneous mass of human labor-power, composed though it be of innumerable individual units. Each of these units is the same as any other, so far as it has the character of the average labor-power of society, and takes effect as such; that is, so far as it requires for producing a commodity, no more time than is needed on an average, no more than is socially necessary.”

Marx next affirms that “the quantity of labor….is measured by its duration, and labor-time in its turn finds its standard in weeks, days, and hours.”[2]

Marx here evades the point. Labor-power and labor-time are totally different concepts. A week, a day, or an hour may constitute a standard unit of time, but not of labor-power. To attempt to measure the expenditure of vital energy with the dial of a clock is tantamount to making an attempt to measure a pound of potatoes with a yard-stick. It is not my design however to engage in a criticism of Marx’s theory of value. For the purpose of exposing the inconsistency between his theory of value and of surplus-value, I shall take the theory of value for granted. I would here remark, nevertheless, that there is all the difference in the world between labor-time as a unit of labor-power. Marx appears to be quite unconscious that any such difference exists.

The exchange-value of a commodity, says Marx, is measured by the average amount of labor-time expended in its production; and while its value varies in direct proportion to the quantity of labor-time, it varies inversely as to the productiveness of labor-time, embodied therein. Thus, if the exchange-value of a commodity is represented by V, and the quantity of labor-time by T, then V varies as T (V ∝ T). On the other hand, if the productiveness of labor-time is represented by P, then the less P enters into the production of a commodity, the greater is T, and therefore V. Contrariwise, the greater is P, the less does T enter into a commodity, and therefore V. V consequently varies, not directly as P, but inversely as P (V ∝ 1/P).

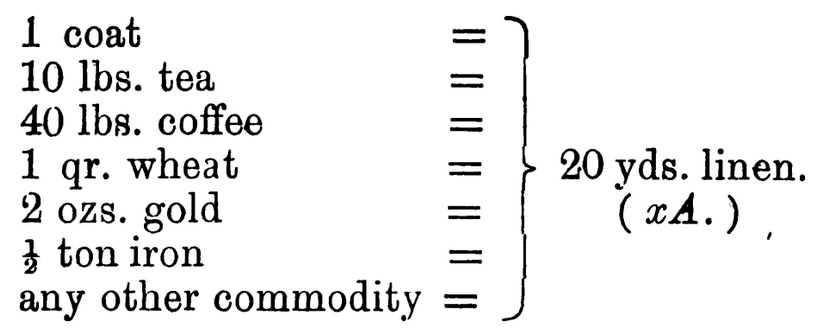

The elementary form of exchange-value is expressed in the relation of one commodity to another of a different kind but of equal value. For example: Suppose xA represents 20 yards of linen, and yB represents 1 coat, and xA=yB. The value of the 20 yards of linen is therefore expressed by 1 coat. This equation is reached by an estimation that the same average total quantity and quality of labor is embodied in each product: other things equal, the same sum total of labor-time has been found to enter respectively into their production. A is the relative form, while B is the equivalent form, of value. The transposition of A and B, as relative and equivalent forms, does not affect the equation.

Let us now consider the developed form of value-relation. 20 yards of linen = 1 coat, or = 10 lbs. Of tea, or = 40 lbs. of coffee, or = 1 qr. Of wheat, or = 2 ozs. of gold, or = ½ ton of iron, or = etc. By precisely the same process of comparison, the value of 20 yards of linen is now expressed in given quantities of various other commodities.

If we consider the converse relation of this developed form, we shall have the following equations:

The values of all commodities are now expressed by the one commodity xA, which has been theoretically transformed into the universal equivalent. Here we have the idea of money in its inception. Either of the commodities was free to figure as the universal equivalent, but gold has ultimately got elected to this office.

We have therefore to consider next the money, or price, form of the value relation:—

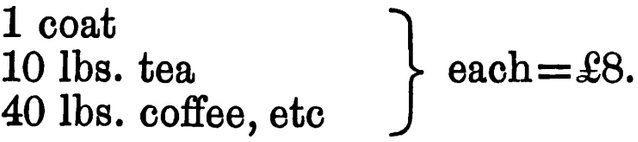

Says Marx: “Gold is now money with reference to all other commodities only because it was previously, with reference to them, a simple commodity.” To be sure; and since the sovereign[3] is but the name of a definite quantity, as a unit, of 11/12 fine gold (123 27447 grs.), two ounces of gold may henceforth figure roughly as £8. We may then vary the last series of equations thus:

II.—The Theory of Exchange.

As we have seen, exchange is a social relation. If a producer offers commodities for sale, it is because they possess no special utility for him, and because they do possess a special utility for others. If therefore he parts with these commodities for the price which represents their cost of production, it is because he is able, in turn, to buy with the money for which he exchanges them, other commodities which have a special utility for him at their cost of production.

It would be superfluous to follow the evolution of exchange which Marx traces in this chapter, inasmuch as its truth does not in the least affect our enquiry into the origin of surplus-value. Suffice it to say that in proportion as exchange extends beyond narrow limits and enlarges its field of operation, labor-time becomes more and more definitely constituted, and the money form naturally passes to those commodities which are best able to fulfil the functions of money; in fine, to the precious metals.

Says Marx: “Up to this point, however, we are acquainted only with one function of money, namely, to serve as the form of manifestation of the value of commodities, or as the material in which the magnitudes of their values are socially expressed. An adequate form of manifestation of value, a fit embodiment of abstract, undifferentiated, and therefore equal human labor, that material alone can be whose every sample exhibits the same uniform qualities. On the other hand, since the difference between the magnitudes of value is purely quantitative, the money commodity must be susceptible of merely quantitative differences, must therefore be divisible at will, and equally capable of being reunited. Gold and silver possess these properties by nature.”

Marx here shews a rare insight into the requisite conditions of a measure of value, or monetary exponent. But he has so far only considered one of the functions of money, that of universal equivalent, which enables us to compare and express the value of all commodities in terms of one of these.

As we have seen, it is not money which makes commodities commensurable, but rather the commensurability of all commodities, in being the visible and concrete exponents of average human labor, which enables one of these, e.g., gold, to assume the rôle of universal equivalent.

The expression of a commodity-value in the language of this universal equivalent is its price. From which it appears that money itself has no price. Its value-relation, nevertheless, remains unaltered.

“As measure of value”, says Marx, “and as a standard of price, money has two entirely distinct functions to perform. It is the measure of value inasmuch as it is the socially recognised incarnation of human labor; it is the standard of price inasmuch as it is a fixed weight of metal”. That these are separate and distinct functions is altogether untenable, for the second function necessarily includes the first; the object of the former is only accomplished by the latter. But we have no occasion to quibble over mere words. As a measure of value, then, gold converts the whole range of commodities into money prices, into ideal equivalent quantities of gold.

No one has more effectively disposed of that financial stupidity which asserts that ideal money may dispense with a commodity unit. “Although the money”, he says, “that performs the functions of a measure of value is only ideal money, price depends entirely upon the actual substance that is money. The value, or in other words, the quantity of human labor contained in a ton of iron is expressed in imagination by such a quantity of the money commodity as contains the same amount of labor as the iron”.

No matter how much or how little the value of gold may vary, different quantities of gold must for ever maintain the same proportion, one to the other. Every change in the value of gold affects all commodities alike, and therefore leaves untouched their relative values, notwithstanding that other commodities may be expressed in higher or lower gold prices.[4] Gold as a standard or measure of value is only an evil when gold is also a medium of exchange, i.e., when contracts and debts have to be settled in fixed sums of gold without taking into account any fluctuation in the value of gold in the interim between the making of the contract and its liquidation.

III.—The Double Function of Money.

What Marx completely overlooked was the fact that when gold became adopted as the medium of exchange it became possessed of an altogether new attribute which inherently it did not contain. As a mere commodity, its consumption was restricted to the arts. It was not in general demand. But everybody wants money. The demand for it is universal. It is a necessity of our complex system of production and exchange. And since the supply of gold is very limited, and out of all proportion to the demand for it as money, its purchasing-power is augmented enormously, bearing no sort of proportion to its normal exchange-value, or cost of production.

As soon as it is conferred upon gold the important distinction of being the only legal tender in the payment of debts, it becomes incumbent that every commodity shall be first exchanged for gold before any other commodity needed can be procured. The owners of gold are thereby enabled to levy a toll on exchange. C—G—C now becomes the general formula for commodity exchange, instead of C—C. C—G is therefore a sale, G—C a purchase; the circulation of the total commodities in society is but a repetition of this process.

Marx furthermore confounded ideal with real money, that is, gold as a measure of value and as a medium of exchange, in considering the effect of money on the circulation of commodities. From which error of reasoning he was led to another, namely, that the quantity of money is ever responsive to the demands of commodity-circulation.

“The value of commodities,” he says, remaining constant, their prices vary with the value (italics mine) of gold (the material of money), rising in proportion as it falls, and falling in proportion as it rises. Now if, in consequence of such a rise or fall in the value of gold, the sum of the prices of commodities fall or rise, the quantity of money in currency must fall or rise to the same extent. The change in the quantity of the circulating medium is, in this case, it is true, caused by the money itself, yet not in virtue of its function of a medium of circulation, but of its function as a measure of value.”

Such angular reasoning as this is well calculated to land its author in the quagmire of sophistry which we shall presently discover him. While it is unquestionably true that a rise in the value of gold will lower the prices of general commodities, and vice versa, it is also equally true that the same result will be obtained from a withdrawal, or augmentation, not only of the quantity of gold in circulation, but of credit instruments. To increase the exchange-value, that is, the purchasing power, of circulating gold it is only necessary to restrict its supply, while every addition to its volume, other things equal, will diminish its exchange-value or purchasing power. Marx innocently supposed that any such withdrawal or augmentation of circulating gold could only result from a rise or fall in its cost of production.

Let us suppose a given sum total of commodity exchanges in a given time. Let us suppose also that the supply of circulating gold is only governed in its quantity by the number of exchanges each piece of gold is able to effect. Let the total number of exchanges be represented by £1000, and the quantity of gold by £100, that is to say, let the relation of money to commodities be as 1 to 10. The prices of the commodities must certainly in such a case be expressed by the quantity of gold. Each sovereign, on an average, will sustain an inseparable relation to ten times its value in general commodities. Now let £50 of gold be suddenly withdrawn from circulation: the prices of the total commodities in that case will only figure as £500 instead of £1000 as heretofore, which will enable the financial class to purchase general commodities at half their former price, while neither the gold nor the commodities in general have in the least varied in their value, or rather, their cost of production.

“If the mass of commodities remain constant,” says Marx, “the quantity of circulating money varies with the fluctations in the prices of those commodities.” He is clearly in error; and it is easy to prove that the opposite of this is really the case. The prices of commodities can only be expressed by a given quantity of gold in circulation, or by means of paper based upon gold that is not in circulation. And the fluctuations in the prices of general commodities only register the fluctuations in the quantity of gold or paper in circulation, if we assume, with Marx, that not only the mass, but the value of that mass, of commodities, remain constant. If, on the other hand, the mass remains constant, and its value augments 50 per cent., the total, say to £1500, then the amount of money (gold or paper) required to effect its exchange, according to our theoretical illustration, will be £150. And if the additional £50 does not enter into circulation, it is self-evident that of two things one; either the total mass of commodities will not be exchanged, or its total price will be forced down to the original total circulating level. Those of us who are actual business men and not mere theorists, know perfectly well how Marx is hopelessly in the wrong. He clearly understood this much, that the exchange of the sum total of commodities depends upon a given volume of money, proportional to its rapidity of movement, but it never appeared to enter his head that the actual quantity of money in circulation sustains no sort of natural or adequate relation to the mass of commodities requiring to be exchanged. Everyone knows to what tremendous proportions modern credit has grown for no other reason than the inability of gold production to keep pace with the production and consequent exchange of all other commodities combined, since the introduction of machinery.

Marx appeared to be overawed by the colossal movements of modern credit, and labored under the manifest delusion that its gold basis played a very insignificant rôle in the distribution of wealth. He completely overlooked, or did not understand, the fact that all credit instruments are not only subsidiary, but tributary, to gold, and that every commercial transaction of this kind has a toll levied upon it by the financial class equal to the rate of interest, whether the gold be present or not.[5]

It is not to be overlooked, moreover, that the volume of credit sustains a certain subjective relation to the quantity of gold coin, or bullion waiting to be coined. As John Law says; “Credit that promises a payment of money cannot well be extended beyond a certain proportion it ought to have with the money.” Is it not apparent that if this were not so we could dispense with gold altogether, even under the present currency system?

From the half-truth that prices vary according to the value of gold, Marx imagined that the quantity of money in circulation depends on the sum total of commodity-exchanges. “The law,” he says, “that the quantity of the circulating medium is determined by the sum of the prices of the commodities circulating, and the average velocity of currency, may also be stated as follows: given the sum of the values of commodities, and the average rapidity of their metamorphoses, the quantity of precious metal current as money depends on the value of that precious metal.” But this is to reason in a circle. It is absurd to suppose that we can assume a sum of commodity values, and their average exchange movements, without a direct reference to the money in terms of which these values and these exchanges can only be expressed. If, however, Marx’s proposition is stated as a minor one, it is true enough. For if the quantity of money in circulation or available for circulation has first determined the number of changes to be effected, then it certainly follows that the circulating money is proportional to those exchanges. Marx confounded the cause and the effect.

“But”, says he, “the erroneous opinion that prices are determined by the quantity of the circulating medium, and that the latter depends on the quantity of the precious metals in a country; this opinion was based by those who first held it on the absurd hypothesis that commodities are without a price, and money without a value, when they first enter into circulation, and that, once in the circulation, an aliquot part of the medley of commodities is exchanged for an aliquot part of the heap of precious metals.” If this is an erroneous opinion, Marx has utterly failed in his attempt to refute it. Neither does this opinion originate in the hypothesis that commodities and money originally meet, the former without price and the latter without value; moreover, its truth is evident from every-day experience. Ask any merchant when prices are low: he will reply, when money is scarce or slow of movement, in a word, when it does not freely circulate. When high : when money is abundant.[6]

At an earlier stage of his inquiry Marx himself declared that simple commodities in circulation are indeed without a price until one of them, e.g., gold, figures as universal equivalent. On the other hand, no single exponent of the quantitative theory of money, as far as I am aware, has ever held the opinion that gold is or was without a value. The holder of such an opinion is simply a man of straw of Marx’s special creation. In a free and normal market, where the demand for and supply of general commodities, including gold, are approximately equal, gold and other commodities will exchange on the basis of their normal value, or cost of production. What is contended, however, is that as soon as gold is set up as an exclusive medium through which the exchange of all other commodities is possible, then the demand for gold becomes as great as that for all other commodities combined; that is to say, the demand is suddenly set up for such a quantity of gold whose value equals that of the sum total of commodities requiring to be exchanged in a given time. Of course the consumption of commodities enables that quantity of gold to effect the same number of exchanges a second time, and so on, until the gold is worn out, but if this natural proportion in the supply of money to the demand for it be not maintained, the purchasing power of money will be altogether disproportionate to its normal value. While its cost of production will remain the same, its exchange-value, that is, its purchasing-power, will rise, and in proportion to the intensity of the demand. Marx supposed that the exchange-value of gold as a simple commodity (before its adoption as money) was identical with the purchasing-power of gold as money. And to maintain his thesis he was logically bound to deny that money is any way subject to the law of supply and demand, which is the reductio ad absurdum of his position.

IV.—The Theory of Capital.

“The simplest form of the circulation of commodities,” says Marx, “is C—M—C, the transformation of commodities into money, and the change of the money back again into commodities; or selling order to buy. But alongside of this form we find another specifically different form: M—C—M, the transformation of money into commodities, and the change of commodities back again into money; or buying in order to sell. Money that circulates in the latter manner is thereby transformed into, becomes capital, and is already potentially capital.”

It cannot possibly be contended that capital has its source in the mere form of circulation, M—C—M. In C—M—C, we have the simple commodity circuit, the definite exchange of one commodity for another by means of a money medium. It is childish to pretend that in M—C—M, the exchange of money for money through a commodity medium, is essentially a different form of circulation, or that it is anything but a connected phase of the same form. But, says Marx, “it is evident that the circuit M—C—M would be absurd and without meaning if the intention were to exchange by this means two equal sums of money, £100 for £100.” In a free market, however, it would be impossible to exchange a commodity for more money than it cost, exceptional circumstances aside. Yet this is what Marx desires to bring home to his readers. “If I purchase 2000 lbs. of cotton,” says he, “for £100, and resell the 2000 lbs. of cotton for £110, I have in fact, exchanged £100 for £110.” To be sure, but a great deal hangs on that little conjunction, if, and political economy is not a science of conundrums.

It may happen, as indeed it often does, that a middleman may know of a market for cotton of which the actual producer is unaware, and in virtue of this superior or accidental knowledge in the matter of markets, he is able to net a profit of £10 by negotiating between seller and buyer. But middlemen are under no moral obligation to furnish commodity sellers with markets gratis, any more than capitalists are under a moral obligation to supply laborers with facilities for production without consideration.

We must not for a moment suppose that capital did not exist before the so-called capitalistic era; or that it did not exist before the invention of money. Therefore, if Marx’s supposition is a correct one, that capital results from the circulation, is there more reason for assuming that it results from the phase M—C—M than from C—M—C? Buying in a cheap market and selling in a dear one is a familiar platitude, but does not the converse hold equally good? Is it not also a familiar platitude that to buy is one thing, but to sell is another?

“One sum of money” is distinguishable from another only by its amount,” says Marx. “The character and tendency of the process, M—C—M is therefore not due to any qualitative difference between its extremes, both being money, but solely to the quantitative difference.” Is this not equally true of the commodity? Is there any qualitative difference in the 2000 lbs. of cotton bought for £100, and the 2000 lbs. of cotton bought for £110? “More money,” says Marx, “is withdrawn from circulation at the finish than was thrown into it at the start.” Not at all; it has simply changed hands. “The cotton that was bought for £100,” says Marx, “is perhaps resold for 100+£10, or £110. The exact form of this process is therefore M—C—M, where M’= M+Δ M= the original sum advanced, plus an increment. The increment or excess over the original value I call ‘surplus-value’.”

Marx here unwittingly states the true process in the creation of surplus-value. But in consequence of an absurd supposition upon his part that it is possible for every producer to sell his commodity for £10 above its value, he concluded that the solution of the problem had not been reached.

V.—Contradiction of the Theory of Capital.

Marx proceeds to point out the discrepancy between the theory and the fact. In theory, he says, surplus-value cannot arise from mere circulation, and yet, on the other hand, we know that it does not arise apart from circulation. We are led to this magnificent exhibition of logic: “It must have its origin both in circulation and yet not in circulation.”!

The problem now is, if surplus-value does not arise from the mere circulation of commodities (and we have seen that its existence contradicts all the previously considered laws which regulate the value of commodities and their exchange), where does it come from? A similar problem puzzled Topsy.

We know very well that if equivalents are exchanged, neither a surplus-value on the one hand nor a minus-value on the other, can possibly arise. Marx proceeds to examine the suppositious case[7] of a non-equivalent exchange.

He says: “Suppose that by some inexplicable privilege, the seller is enabled to sell his commodities above their value, what is worth 100 for 110, in which case the price is nominally raised 10%. The seller therefore pockets a surplus-value of 10. But after he has sold he becomes a buyer. A third owner of commodities comes to him now as seller, who in this capacity also enjoys the privilege of selling his commodities 10% too dear. Our friend gained 10 as a seller only to lose it again as a buyer. The net result is, that all owners of commodities sell their goods to one another at 10% above their value, which comes precisely to the same as if they sold them at their true value.”

It requires no argument to show that surplus-value cannot possibly arise from the exchange of equivalents. This is self-evident. Neither is it to be denied, Marx to the contrary notwithstanding, that surplus-value arises from any other source than the exchange of non-equivalents. It therefore follows that Marx, in dismissing the idea that surplus-value does actually arise from the exchange of non-equivalents, has failed to comprehend the problem of surplus-value, far less to furnish its solution. It is of course perfectly obvious that if all producers sell their commodities at 10% above their value, it is as though they sold them at their true value, since value is essentially a relation. But here Marx utterly begs the question.

In order to demonstrate that surplus-value arises from the exchange of equivalent values, Marx would have to invest the term, surplus with a totally different meaning from what is properly is algebraical equivalent.

Indeed, this he does, and therefore all his professedly algebraical demonstrations go for nought. The term, surplus, employed in this connection, necessarily implies a relation of minus. In the exchange of 100 for 100, 100=100, it is mathematically impossible that it can be 100=110 by any theoretical explanation whatever. Nor can the equation be otherwise than either

The conclusion is therefore irrestible—and the merest schoolboy could have corrected Marx in this—that if in the exchange of two given value quantities there is a surplus-value of 10% on the one side, there is a minus-value of 10% on the other.

Instead of making the least attempt to demonstrate the silly proposition that surplus value arises in and by the exchange of equivalents (wherein he was probably conscious of his own weakness), he attempts to shift the onus of proof altogether by calling up for consideration some hypothetical objection to that proposition.

“To be consistent,” he says, “the upholders of the delusion that surplus-value has its origin in a nominal rise of prices or in the privilege which the seller has of selling too dear, must assume the existence of a class that only buys and does not sell, i. e., only consumes and does not produce. The existence of such a class is inexplicable from the stand-point we have so far reached, viz., that of simple circulation.”

Marx now gives himself away. He has completely shifted his ground. In the first place, he has been considering, not simple circulation at all, but commodity plus money circulation, a totally different thing. It is true he regarded money as a simple commodity, but, as we have seen, he was in this respect guilty of a mere assumption of which only a person possessing an incomplete acquantance with the subject of money could possibly be guilty. The standpoint reached was the circulation of commodities by means of money. Let me remind the reader that surplus-value did not appear until money came upon the scene. But Marx’s vision was too clouded by preconceptions to perceive the full significance of that fact.

Marx’s theory excludes the elements of rent, interest, and profits from the category of value. Rent is attributed to the legal monopoly of land tenure, and interest is attributed to the monopoly of capital (Marx here confounding capital and money, that is to say, the thing acquired and the means of acquisition). He did not understand that profits were wholly contingent upon interest, except where they result from an advantage (mental or other) which its recipient possesses over the marginal producer. The supposition that interest is due to any other form of capital than gold credits is not to be entertained for a moment. It is only this particular form of capital, through means of which all other forms of capital are obtainable, that commands a premium known as interest. The operation of competition upon all other forms of capital renders it impossible for them to command such premium. Whoever heard of a wheelbarrow being invested at 5 per cent? Bastiat made a futile effort to maintain a similar proposition, but he held to no such theory, as Marx and I hold in common, that the value of commodities varies in inverse proportion to the productiveness of labor.

Nevertheless, will Marx seriously maintain that the recipients of rent and interest do not constitute “a class that only buys and does not sell, i. e., only consumes and does not produce”? To affirm that such a class (not to speak of an equally large class of state sinecurists and pensioners) is inexplicable from the standpoint reached, is the merest subterfuge. Furthermore, patent, copyright, licence, tariff laws or custom duties, protective restrictions in general, easily explain the fact that one producer may sell his product too dear while another is deprived of that privilege.

Now, since the consumer is entirely in the hands of the producer, the latter is able,—but proportionately to the intensity of the demand for his product,—to raise prices to whatever extent he pleases. The actual corrective is competition amongst the producers. The producer, to be sure, is under the necessity of enhancing the prices of the products he sells above the labor-cost of selling them in order to recoup himself for the rent, taxes, etc. of shop or warehouse, and interest upon the money, if borrowed, that furnished his capital or stock. But as he naturally desires to turn over his goods, he is bound, by the exigencies of the situation, to offer them at a price which corresponds with the purchasing power of his customers. If he is a distributor proper, and the producers are his only customers, then the prices of commodities will, thanks to competition, be represented by their cost of production and distribution. But, as we have already observed, there is another class which does not labor, and which subsists upon rent, interest, and taxes. Prices consequently, when reduced to their minimum by competition, are not governed by the wages of the producers and of the distributors, but by the sum of wages, rent, interest (and profits contiguous thereto), and taxes.

VI.—Labor-Power as a Commodity.

Reviewing his previous conclusions, Marx affirms that the origin of surplus-value is not to be found in money. It therefore follows, he says, that the change of value expressed in the formula M—C—M + surplus-value, arises from the commodities themselves. It cannot be effected in the phase C—M of the circuit M—C—M. It must therefore be effected in M—C, and in C, since it does not take place in M.

It is admissible in the realm of deductive logic to state as a right conclusion that which is presented as one of two or more alternatives, when that one is incompatible with the remainder, and the remainder are proved to be wrong. But when your theorist has omitted from consideration an important factor in the case (i.e., the difference between the normal value of gold as a simple commodity and its purchasing-power as money) which, if included, would not have justified the positing of any such alternatives, then there is a difference. The change of value does not originate in money, says Marx, and “we are therefore forced to the conclusion that the change originates in the use-value, as such, of the commodity, i. e., in its consumption.”

One would naturally suppose that the consumption of a commodity, instead of being a source of surplus-value in exchange, occasion- ed the extinction of value altogether. If I purchase a pair of boots at the market price, and wear them out, body and sole, I am certain that I should experience some little difficulty in selling their remains for more than I paid for them originally. If I purchase a beef-steak, and with more or less difficulty manage to digest it, I am positive that its exchange-value is a thing of the past, not to speak of a surplus-value. By what extraordinary freak of nature, then, can the consumption of the use- value of a commodity give rise to surplus-value?

Let Marx explain. “In order to be able to extract value from the consumption of a commodity, our friend, Moneybags, must be so lucky as to find, within the sphere of circulation, in the market, a commodity whose use-value possesses the peculiar property of being a source of value, whose actual consumption therefore is itself an embodiment of labor, and consequently, a creation of labor. The possessor of money (italics mine) does find on the market such a special commodity in capacity, for labor or labor-power.”

Preposterous! This fable of Marx’s completely eclipses the fable of the Phoenix! Having searched in vain for an ordinary commodity whose consumption is a re-incarnation of itself with a surplus to boot, he could do nothing better than invent one for the express purpose, man of resources that he was. Labor-power a commodity! What an outrage on reason!

Marx has already led us to the following conclusions:

(1.) That a commodity is an object upon which labor (the application of labor-power) has been expended;

(II.) That the use-value of a commodity does not enter into its exchange-value.

1. How can labor-power be classified as a commodity on Marx's own showing? If labor is an effect of labor-power, and a commodity is an effect of labor, by what process of logic can the conclusion be reached that labor-power is a commodity? O sophist, hide thy diminished head!

II. If the use-value of a commodity has nothing whatever to do with the exchange-value thereof, why, in the name of common sense, is the use-value of the “commodity” labor-power an exception to the rule? We are now able to see that Marx’s theory of surplus-value is consequent upon the following inconsistent proposition: A commodity is both a cause and an effect of labor, whose use-value does, and at the same time does not determine the measure of its exchange-value!

We are here brought face to face with a contradiction so unmistakeable, so absolutely palpable, that no trick of dialectical legerdemain shall ever reconcile it.

“But,” says Marx, “in order that our owner of money may be able to find labor-power offered for sale as a commodity, various conditions must first be fulfilled. The exchange of commodities of itself implies no other relations of dependence than those which result from its own nature. On this assumption, labor-power can appear upon the market as a commodity, only if, and so far as its possessor, the individual whose labor-power it is, offers it for sale, or sells it, as a commodity. In order that he may be able to do this, he must have it at his disposal, must be the untram- melled owner of his capacity for labor, i. e., of his person. . . He and the owner of money meet in the market, and deal with each other as on the basis of equal rights, with this difference alone, that one is buyer, the other seller ; both, therefore, equal in the eyes of the law.”

We have seen that the essential functions of money are two; one, that it shall represent a definite commodity-quantity as a unit; the other, that it shall serve as a medium of payment. We have seen, furthermore, that the first function arises from the nature of things. We have also seen, on the contrary, that the exclusive investment of gold with the second function is an act of financial despotism. There is no valid reason why the same commodity should perform the two functions, nor why the second function should be confined to one commodity. Indeed, to so confine it is to make of money a monopoly, and the monopoly of money means practically the monopoly of everything else which can only be purchased with money. Gold henceforth becomes the emperor of commodities, the autocrat of ex- change. He who possesses gold possesses not only a commodity, but money, the god before whom all commodities bow. The owner of money enters the market, not as a mere producer of commodities in general, but as the owner of a preferential commodity. It cannot be pretended that the same competition takes place with regard to the supply of gold as with regard to the supply of commodities in general. The law of supply and demand therefore invests gold with a premium; and to say that gold is at a premium in the table of values is only to say that in relation to it all other commodities are at a discount. What utter nonsense, then, for Marx to assert that the laborer and cap- italist enter the contest of the market both equally equipped.

“The continuance of this relation,” he proceeds, “demands that the owner of the labor-power should sell it only for a definite period, for if he were to sell it rump and stump, once for all, he would be selling himself, converting himself from a free man into a slave, from an owner of a commodity into a commodity.”

Is not this the subtlest of metaphysical distinctions, that the laborer is a slave if he sells himself outright, but a free man if he sells himself piecemeal? What has the length of the lease to do with his moral status?

“The second essential condition to the owner of money finding labor-power in the market as a commodity," says Marx, “is this —that the laborer, instead of being in the position to sell commodities in which his labor is incorporated, must be obliged to offer for sale as a commodity that very labor-power, which exists only in his living self.”

Now, Marx has just told us that one essential condition of finding labor-power on the market as a commodity is that the laborer, its possessor, freely offers it as such, and that in doing so, he stands upon an equal footing with the capitalist.

“He and the owner of money meet in the market, and deal with each other as on the basis of equal rights, with this difference alone, that one is buyer, the other seller; both, therefore, equal in the eyes of the law.”

And yet in the same breath Marx calls upon us to believe that the other indispensable condition of finding labor-power on the market as a commodity is that the laborer is obliged to offer it as such! This extraordinary right-about-face is only to be equalled by Æsop’s fable of the Man and the Satyr. One thing is quite evident, that Marx was unable to agree with himself for five minutes together.

To entertain the opinion that labor-power is a commodity is about as absurd a length to which a man, professing to understand the rudiments of economic science, could possibly go. But when the originator of that opinion ventures to furnish an argument in substantiation thereof by mixing up the commodity itself with the moral rights of the owner of that commodity, and fails to produce a better argument than this—that in order that labor-power may appear as a commodity, it is necessary that its owner shall in the first place be, and in the second place not be, a free agent—it is safe to assume that such a man has become mentally impoverished indeed.

Let us, however, proceed. Marx next discusses what are the essentials of capitalistic production. “In order,” he says, “that a man may be able to sell commodities other than labor-power, he must of course have the means of production, as raw material, implements, etc.” The obvious inference is that the Capitalist, having a monopoly of these things, is thereby enabled to compel the laborer to accept a commodity price for his labor, or starve.

But the question naturally arises—how did the capitalist become possessed of these things which constitute his capital, if the laborer produced them? “Capital”, says Marx, "can spring into life, only when the owner of the means of production and subsistence meets, in the market, with the free laborer selling his labor-power.” But this is to beg the question. The owner of the means of production and subsistence is the owner of capital. Then why did not Marx strip the argument of all verbiage and reduce his proposition to the bald statement that capital can spring into life only when the owner of capital meets, in the market, with the free laborer selling his labor-power? That would have been too glaring, and like the hypothesis of a First Cause, it would have explained nothing.[8] Notwithstanding, Marx has put himself into a logical quandary from which there is no escape. He manages to hold to these antithetical propositions at one and the same time:—

I. That capital is an effect of surplus-value;

II. That surplus-value is an effect of capital.

It was once queried which was first, the chicken or the egg. Marx would have solved that enigma very easily: he would have said—both.

In order to corroborate the contention that labor-power is a commodity, he attempts to shew that its value is actually determined, like that of any other commodity, “by the labor-time necessary for the production, and consequently also the reproduction, of this special article. . . The value of labor-power is the value of the means of subsistence necessary for the maintenance of the laborer”.

But where is the analogy? The sum total of the factors in the production of a commodity, in other words, its value, and the cost of reproducing one of such factors, viz., the labor-power exerted, are two entirely different things. Not only are they different in degree, but in kind. The capitalist does not buy labor-power, which is inert labor, but labor pure and simple. What is the use-value of labor-power apart from its application? Marx got into a hopeless muddle when he found himself called upon to discuss the cost of the laborer’s production. For who is able to estimate the labor which he cost to the mother who bore him, who nurtured him, and fitted him to labor in his turn? By what law of economy is all this to be adequately calculated in terms of that quantity which simply prevents him from starving? Does the value of the steam-engine sustain any sort of relation to the cost of the coal that feeds it?

O economic wiseacre! Do you not see that your conclusion is self-evidently absurd? that it involves the proposition that the total product of labor in a given time is only equal to a part thereof, and that part just so much as necessity compels the laborer to consume in that given time? Does not the laborer produce very much more than he consumes? Very well; then, if, hypothetically, all men are laborers, governed by the same circumstances, to whom shall the surplus-product belong?

As a matter of fact, however, wages are not governed by the necessities of the laborers. In some cases, wages are actually lower than the maintenance of the laborer’s necessities, and the cry has gone forth for a living wage. We have to consider the average condition of wages, however, and in that respect it may be said that while the absolute needs of the laborer are practically a fixed quantity, wages, on the other hand, have been rising above that point continuously since the introduction of machinery.

It is a fact that the average prices of those commodities which are the most necessary for the laborer’s subsistence have steadily fallen during the last half century, while the average nominal wages have steadily risen in the same time. Thus, if machinery has displaced laborers, and pushed them into a new field of enterprise, it has at the same time raised the wages of labor (both nominal and real), and not, as Marx assumes, brought into play an opposite tendency.

VII.—The Process of Producing Value and Surplus-Value.

“Let us now return,” says Marx, “to our would-be capitalist. We left him just after he had purchased, in the open market, all the necessary factors of the labor process; its objective factors, the means of production, as well as its subjective factor, labor-power. With the keen eye of an expert, he has selected the means of production and the kind of labor-power best adapted to his particular trade, be it spinning, bootmaking, or any other kind. He then proceeds to consume the commodity, the labor power, that he just bought, by causing the laborer, the impersonation of that labor-power, to consume the means of production by his labor. The general character of the labor-process is evidently not changed by the fact that the laborer works for the capitalist instead of for himself.” Marx further points out that this process adds only two new features to the natural process; one, that the capitalist directs the labor, or the application of the labor-power, he has bought; the other, that he owns the total product. The capitalist is therefore to be considered as a middleman between the producer and the consumer.

“Our capitalist,” Marx proceeds, “has two objects in view: in the first place, he wants to produce a use-value that has a value in exchange, that is to say, an article destined to be sold, a commodity; and secondly, he desires to produce a commodity whose value shall be greater than the sum of the values of the commodities used in its production, that is, of the means of production, and the labor-power that he purchased with his good money in the open market. His aim is to produce not only a use- value, but a commodity also; not only use-value, but value; not only value, but at the same time surplus-value.” But on the hypothesis that all commodities exchange on the basis of the cost of production of the labor-time consumed in bringing them into existence and upon the market, this is impossible. Marx, however, is not in the least dismayed on that account, and proceeds to the demonstration.

He sets forth, firstly, a theoretical case of production from a value point of view. Cotton (the raw material) is to be transformed into yarn (the commodity). The value of one hour’s labor is taken at 6d. The wear and tear of implements is reckoned at 2s. Let 10 lbs. of cotton, worth, say 10s., be transformed in 6 hours into 10 lbs. of yarn. Then it is manifest that if we leave the element of labor out of account we have embodied in the commodity, a value of 10s.+2s.=12s. Then 6 hours of labor at 6d. an hour, expended in bringing about this result, amounts to 3s. The total value of the commodity (10 lbs. of yarn) is therefore 10s.+2s.+3s.=15s.

But yarn can be bought in the market at 1s. 6d. per lb., or 10 lbs. for 15s., says Marx. Precisely, if it is sold at a price representing its cost of production.

From this theoretical consideration we now pass on to what Marx calls a real case. The Capitalist has discovered, says Marx, that the cost of the daily maintenance of the laborer is 3s. whether he works 6 hours or 12. And it is upon this extraordinary presumption that Marx rests his “real case.”

It must be obvious to the meanest mind that if the cost of labor for 12 hours is 3s., its cost for 6 hours will be 1s. 6d. Then by what reason did Marx assume, in the theoretical case just considered, that 3s. was the value equivalent of 6 hours’ labor? For was it not an essential presumption on his part that the laborer's wages should be calculated on the basis of the cost of production, that is, the means of subsistence? Either 3s. for 6 hours’ labor was too much, or 3s. for 12 hours’ labor was too little. No dialectical shuffling can controvert that. And so Marx attempts to demonstrate the truth of an impossible proposition by twisting the terms of his argument.

Profound logician!

Let us proceed to examine Marx’s “real case”. The capitalist has the means of production necessary to employ the laborer, not 6 hours, but 12. Instead of 10 lbs. of cotton, there are 20 lbs., worth 20s. The wear and tear of machinery will also be double in 12 hours than in 6, so this must be represented by 4s. The laborer receives 3s., as in the previous case, but for 12, instead of for 6 hours.

The capitalist's expenditure, therefore, is now as follows: 20s. (cotton) +4s. (wear and tear of plant) +3s. (labor) =27s.

But, says Marx, that gives him 20 lbs. of yarn, which at the market price sells for 1s. 6d. a lb. His receipts, therefore, are Is. 6d. x 20 =30s.

A very pretty story; let us look into it more closely. “The value of a day’s [italics mine] labor-power,” says Marx,”amounts to three shillings, because on our assumption half-a-day’s [italics mine] labor is embodied in that quantity of labor-power, i. e., because the means of subsistence that are daily required for the production of labor-power, cost half-a-day’s labor.” The value of commodities, says Marx, is determined by their cost of production; the daily value of labor-power is 3s., because 3s. represents the value of other commodities which cost half a day's labor to produce! Marx furthermore contends that the cost of maintaining labor and the value of labor are totally different value-quantities. But upon such a supposition, what becomes of the theory that the value of a commodity is equal to its cost of production?

“The past labor that is embodied in the labor-power, and the living labor that it can call into action; the daily cost of maintaining it, and its daily expenditure in work, are two totally different things. The former determines the exchange-value of the labor-power, the latter is its use-value. The fact that half-a-day’s labor is necessary to keep the laborer alive during 24 hours does not in any way prevent him from working a whole day. Therefore, the value of labor-power and the value which that labor-power creates in the labor-process, are two entirely different magnitudes.”

Now, if the cost of maintaining labor-power is its exchange-value, by what manner of reasoning (keeping in view that the exchange-value of a commodity is governed by its cost and not in any way by its use-value) can there arise a value of a greater magnitude in the mere application of that labor-power? Will Marx pretend that labor-power not in action has any value at all? Is not its value absolutely contingent upon its application? To come to the point, then, labor-power, as such, has no economic value whatsoever, and the economic distinction which Marx confounded with the mere physiological distinction between labor-power and labor is completely destitute of foundation in fact.

If half-a-day’s labor is necessary to keep the laborer alive during 24 hours, that fact, to be sure, in no way prevents him from working the whole day. But, presupposing Marx’s assumption of a free market, if he work the whole day, he will get as his reward, not half-a-day’s pay, or what is the same thing, half the product. of his neighbour’s whole day's work, but an equivalent of what he has produced, unless he happen to fall amongst thieves. What in the name of reason has his means of subsistence to do with the matter, except as a starting point in the comparison of values? Is there, in a free market, one law for the producers of exchange-values, and another for the purchasers thereof? Is the law of competition, like Janus, two-faced, that it compels the laborer to accept half-a-day’s pay for a whole day’s work, without enabling him to purchase his means of subsistence at half price?

But Marx goes on apparently oblivious of the sea of logical difficulties in which he is submerged. “The useful qualities that labor-power possesses, and by virtue of which it makes yarn or boots, were to him nothing more than a conditio sine qua non; for in order to create value, labor must be expended in a useful manner. What really influenced him (the capitalist) was the specific use-value which this commodity possesses of being a source not only of value, but of more value than it has itself.”

If we pay no attention to the absurd hypothesis of Marx’s that surplus-value arises by reason of the capitalist and not the laborer possessing the means of production; if we also dismiss for the moment the more intelligible supposition that its origin is inherent in money; then the only possible inference to be drawn from the foregoing is that the laborer himself is deficient in the requisite ability to produce value and surplus-value, and the function of the capitalist is necessary to that end. Either this or the laborer cannot find a market. In either case the capitalist must be presumed to supply this deficient ability: he is therefore an essential factor in production and distribution, and the surplus-value he is thus instrumental in creating, is but the equitable reward of his ability and labor, since its rate is governed by competition amongst capitalists. But this is a conclusion which by no means squares with the theory of Marx.

He says: “The use-value of labor-power, or in other words, labor, belongs just as little to its seller, as the use-value of oil after it has been sold belongs to the dealer who has sold it.” But the cases are not analogous. Marx has declared over and over again that the use-value has nothing whatever to do with the magnitude of exchange-value in a commodity.

And yet we are now called upon to believe that, owing to a difference in the respective use-values of labor-power and labor, the capitalist, in purchasing the element of labor-power in a free market at its proper exchange. value, in paying for it a quid pro quo, and in combining other elements therewith which he has similarly bought, is able to command, in the self-same free market, a value ab extra; a surplus-value independent of the value which the labor expended in bringing these several elements into combination occasions; a value greater than the sum of its respective parts!

The commodity, as we have seen, must of course have a use-value in order to have an exchange-value. But inasmuch as the whole force of Marx's contention, viz., that surplus-value is derived from the use-value of commodities as products of labor, depends on the supposition that a free market is maintained, his thesis proves too much. For it involves the absurd idea that labor-power has in point of fact, two use-values which are economically distinct; one which is potential and which ensures its exchangeability on the basis of the means of subsistence, the other, that the laborer is able to impart to his product an additional use-value which creates, in con- sequence, an additional exchange-value.

If the exchange-value of labor-power is fixed by the cost of its production, or maintenance, then it logically follows that whatever the productive magnitude of labor-power, in other words, no matter what is the quantity the laborer is able to produce, the exchange-value of the product of a day’s work, is only equal to the value of the laborer's means of subsistence for that time. How can his labor be susceptible of two exchange-values, on the contrary supposition? If we assume, with Marx, that the laborer's wages are properly (that is, according to the laws of commodity exchange) determined by the means of subsistence, then the capitalist obviously does not exploit him in the productive process at all. Then, if we likewise assume with Marx that the capitalist adds nothing to the total product in that process, we are bound to assume further one of two things: either the capitalist exploits the laborer as a consumer, that is, in charging the laborer for the product of his labor more than it cost him, or the capitalist possesses the extraordinary faculty of being able to create something out of nothing! Ex nihilo nihil fit.

But the simple explanation of the process is unwittingly revealed by Marx himself. On his own shewing, the capitalist, in paying the laborer 3s. for 12 hours’ work, did not pay its proper exchange-value. He has already told us that 3s. represents that quantity of gold in which, not twelve, but six hours’ labor are embodied.[9] Here is the complete solution of the problem. In the exchange of labor for money, the laborer has given a value equal to 6s. for a value which is the monetary equivalent of 3s.

The conclusion we have reached therefore admits but of one explanation in fact, although it admits of two explanations in form. These two explanations may be resolved as follows:

-

The laborer, in selling his labor to the capitalist, sells it below its normal value or;

-

The capitalist, in selling the product of that labor to the laborer, sells it above its normal value.

Since the price expression of value is merely a relation, either of these propositions comes to the same thing. And by reason of this, we are bound to negative Marx’s conclusion that all along the line equivalents have been exchanged for equivalents.

I do not here propose to deal with the moral considerations with which Marx invests his theory of value. They are utterly irrelevant. I hold that no producer is under any moral obligation to produce commodities for others at all. Moreover, if there be any moral right in the matter, it is clearly the producer who is entitled to fix the price of his product. The fact that competition (so detested by the Socialists) does, generally speaking, operate to limit prices and make something like an equality of values possible, is nothing to the point.

If the supply of capital were free, that is, if the power of money to command interest were to cease, by means of which capital could be furnished at the cost of production, then surplus-value would vanish. Any excess of price over cost under such circumstances could only appear as the natural wages of ability. Given a free market, in which capital is just as easily accessible to the laborer as to the capitalist, then, if the laborer is deficient in the ability to organise his own labor and the capitalist does him a service in making good that deficiency, the latter is clearly entitled to any excess of price over cost which he is able to obtain either by the supply of ability or by mere speculation, under the regime of free competition. To deny this is tantamount to saying that ability is not a factor in the case, and Marx’s own distinction between simple and complex, between skilled and unskilled, labor, has no longer the slightest significance.

In conclusion, Marx, quite satisfied that he has supplied the key to the enigma of surplus-value, is emboldened to declare:

“Every condition of the problem is satisfied, while the laws that regulate the exchange of commodities have been in no way violated. Equivalent has been exchanged for equivalent. For the capitalist as buyer paid for each commodity, for the cotton, for the spindle and the labor-power, its full value. He then did what is done by every purchaser of commodities : he consumed their use-value. The consumption of the labor-power, which was also the process of producing commodities, resulted in 20 lbs. of yarn, having a value of thirty shillings. The capitalist, formerly a buyer, now returns to market as a seller, of commodities. He sells his yarn at eighteen pence a pound, which is its exact value. Yet for all that he withdraws 3 shillings more from circulation than he originally threw into it.”

We have already shewn that the conclusions, of which the foregoing passage is a resumé, are at once illogical and contradictory. That a man, professing to understand the rudiments of logic, should affirm that the value of commodities is represented by the labor-cost of all parties in their production, on which hypothesis 10 lbs. of yarn are worth 15s., and then to affirm at the same time that 20 lbs. of yarn are equally worth 30s., with a reduced cost in labor-time of 3s., is to pronounce his own condemnation for all time as a sophist of the most vulgar order.

Obviously, 20 lbs. of yarn produced under conditions of a lesser labor-cost of 3s., will only sell for 27s., if we argue, as Marx does, on the hypothesis of a free market. Marx fell into the error of supposing that 20 lbs. of yarn would sell at the same rate as before, in considering the process of production, not from the social point of view, but from the point of view of a single producer. It was a similar error upon which Bastiat constructed his oft-quoted, but nevertheless utterly stupid, justification of interest.

It is true that society is but an aggregation of capitalists and laborers. But in society, whereas in isolated production it is not the case, the law of competition in production operates without partiality in the determining of prices. Marx’s “real case” recognises, plainly enough, the effect of competition on wages, but completely ignores the existence of any such effect on prices.

Consider:

If, in a given time, the normal demand for yarn, expressed by the needs of the capitalist and the laborer together with their respective families, is 10 lbs., neither more nor less, how can the capitalist, by doubling his output, and reducing the laborer's (that is, his customer's) wages by half, find a market for it? Where are the buyers to come from? And how, by the mere multiplication of capitalists and laborers, by the mere enlargement of the same conditions, is the case any different?

If we return to the first chapter of Marx, he admits without equivocation that while the value of a commodity varies in direct proportion to the quantity of labor-time, it varies in inverse proportion to the productiveness of labor-time, materialised in it. And in passing, this proposition at once clearly and effectively disposes of the proposition of Marx that labor-power is a commodity, for it is nothing more than a plain statement that wages and the prices of the products of labor are governed inversely by the same law.

Now, what is the meaning of the law that the value of a commodity varies in inverse proportion to the productiveness of the labor materialised in it?

Let us suppose that a capitalist employs 20 men, say, in the manufacture of boots by hand. Their output, we will say, is 40 pairs in a week. The weekly wages of each man we will assume to be 20s. Reckoning £10 for raw materials and other elements of cost, of 40 pairs of boots, the total cost in the production of 40 pairs of boots will therefore be £30, or 155. a pair. Let us furthermore assume that the present market price of boots is 22s. 6d. a pair; the capitalist's rate of profit, in that case, is 50 per cent. This rate of profit we will assume to be the normal rate under the conditions presupposed.

Now let a new state of things arise. Machinery is introduced into the boot-making industry, which necessitates a division of labor. The capitalist thereupon surveys the situation, Obviously, if the average demand for boots equals 40 pairs a week, the extra quantity which, thanks to machinery, the laborers are able to turn out, will become dead stock. But the capitalist quickly perceives a way in which he can combine philanthropy and self-interest, which is in keeping with the fitness of things. He sees quite plainly that by cheapening boots, he can sell more of them, and at the same time, fewer people will trudge barefoot: the demand for boots will go up precisely because their price has gone down. He then sets to work 40 men, giving each of them the same wages as before for the same number of hours' work, [10] who are able to turn out 200 pairs of boots in a week. What is the inevitable result? Simply this: that, if we allow, on the basis of our previous calculation, that the capitalist has spent £50 for raw materials, £10 for wear and tear of machines, and £40 for wages, the bootmaking industry has in- creased in productiveness, operating to bring down, by competition, the price of boots to such a sum as will still furnish a profit of 50 per cent., if, as according to our previous supposition, that is the normal rate as governed by interest.[11]

Boots are henceforth sold at 15s., and no longer at 22s. 6d. a pair. And as machinery enters into the productionof other commodities, so the general laborer, in his capacity of consumer, derives a corresponding advantage: if his nominal wages remain stationary, their purchasing power will continually tend to increase. If this increase is not already so apparent as we should be led to expect at the present time, it is simply because the laborer's standard of comfort has been raised slowly and almost imperceptibly, his consumption has been enlarged, and he is suffered to be unemployed for a greater portion of his time than was originally the case. It has been shewn that it is only the monopoly of monetary credit which makes involuntary idleness possible. The idea that it is a natural effect of an over- production can no longer be contended. The more goods are produced, the greater is the quantity called into requisition, to exchange for them, if we regard production apart from the disturbing influence of money.[12]

If involuntary idleness were a thing of the past, it is easy to see that not only would the laborer's power and opportunity of consumption be increased to a degree equal to his present lack of opportunity to labor, but the abnormal competition amongst laborers to secure what is under present circumstances a monopoly of labor would be destroyed, and as a direct consequence thereof, wages would rise to their true maximum. The remedy for this anomalous state of things is simple, and consists in the repeal of those legislative enactments (the legal tender laws) which restrict free competition in the supply of monetary credit.[13] It does not call, by any means, for that drastic and arbitrary treatment which the Socialists appear to think is inseparable from its solution, and which would occasion a revolution of not only the prevailing industrial and commercial conditions, but of our whole social life. The future therefore depends on a larger extension, and not on a limitation, of free-trade principles; the Socialistic idea is merely the logical out- come of the policy of Protection.

What, under the present politico-economic system, divides the industrial and commercial groups into capitalists and laborers is the simple circumstance that the former possess the commodity gold, and gold credits, while the latter do not. The line of demarcation cannot of course be minutely drawn, any more than such a line can be drawn between a class that is rich and a class that is poor, since there are many who are in the centre of these extremes and whose incomes are more or less balanced between a minimum of wealth and of poverty. Nevertheless, the fact remains that there is a capitalist class as well as a laboring class.